TABLE OF CONTENTS

- Summary

- BACKGROUND - TECHNICAL: point 1: decease estate, point 2: the executor

- POINT 1 Decease estate - Info and steps

- POINT 2 THE EXECUTOR OF THE LATE [PERSON NAME] - info and steps

- ______________________________________________________________

- BELOW ARE CHRIS NOTE ON PREVIOUS CASE

- Chris Norris (Jenni)

- ROCKLIFF, SEINI (vivian case)

- ATO call

- Examples

Summary

When someone dies, you need to

- do final tax return called "The executor for the late <client name>"

- MUST notify ATO all of the following:

- via Australia post:

- notify death of client with death certificate (certified copy)

- notify nomination of LEGAL PERSONAL REPRESENTATIVE (LPR). That LPR needs to go to Australia post with certified copies of the grant of probate or letters of admin -

- the LPR is normally the lawyer or the next of kin that is named in the grant of probate / will or letters of administration. IT IS NOT TAX AGENT

- LPR to nominate us in the same form they used to go to Australia (if they don't, its okay, you can add them on TAP normally AFTER LPR has gone to post office).

- via Australia post:

Deceased Estate tax return (trust entity) is for dead clients that still earn income after death (like they had a rental property). Not all dead clients need to do a decease estate tax return.

BACKGROUND - TECHNICAL: point 1: decease estate,

point 2: the executor

There will be two TFN/ two tax return matters for:

Point 1: Deceased estate - tax return matters AFTER DEATH (Definition: A deceased estate is a temporary, separate legal entity created upon a person's death to manage their assets and liabilities until final distribution)

and Point 2 the executor for the late [person name] -

- This one contains the tax returns matter when they were still alive

- there maybe ATO held refund money still owed to them that the late client didn't receive

- Itit contains the late member's super details and previous correspondence history

| Return | Taxpayer | Period |

|---|---|---|

| Final individual return | The deceased person | Start of tax year → date of death |

| Estate tax return | The deceased estate | Date of death → estate distribution |

For up to 3 years, a deceased estate often receives individual tax rates (not trust rates), which can reduce tax.

POINT 1 Decease estate - Info and steps

A. TT office to apply TFN for the DECEASED ESTATE by:

- Using the form (see attachment) or

- The link: https://www.abr.gov.au/tax-professionals/applying-other-registrations/apply-tfn-your-client

- The TFN application can be done at any time; you don't need to wait for LPR to nominate us as a tax agent.

- Please review the form in advance to gather the required information required from: will/ grant of probate/ letter of administration/ etc.

B. Lodge a final tax return for the DECEASED ESTATE

POINT 2 THE EXECUTOR OF THE LATE [PERSON NAME] - info and steps

A. TT will lose access to our client tap once they die

- TT OFFICE WILL HAVE NO MORE ACCESS TO THE DECEASED TAP ACCOUNT

- Tax agent formal representations cease at the time of death

- When the client passes away, a tax agent's automatic authority to act on their behalf ceases immediately, and WE ARE removed from the ATO systems. The agent must be re-appointed by the legal personal representative (LPR/ Executor)

You can add them back to TAP (Chris noted) to view their records. Please note there will be limited functions

B. FIRST THING TO DO -> CHECK IF LPR WAS NOMINATED

go to TAP-> authorised contact or call ATO

If no L,PR nominated next step -

>>>>> contract client to see who is the LPR -> whoever this is they need to nominate with ATO they are LPR

>>>>> if laywer is LPR -> ask them to do it the lawyer can do it

>>>>> if laywer refused to do can send the client this procedure to tell them to notify to ATO Helpdesk : Teresa Tran & Associates

C. LPR (EXECUTOR) TO REAPPOINT TT AS THE TAX AGENT FOR THE EXECUTOR FOR LATE [PERSON]

- Definition = LPR = Legal Personal Representative = person who is authorised to manage a deceased person's estate, including final tax returns, debt payment and assets distribution (example tax return refund).

- The LPR is usually:

- the executor named in the will

- or an administrator appointed by the court.

- The LPR needs/must to notify the ATO that they are managing the estate and appoint us as the tax agent if they wish us to assist with all the deceased's estate tax affairs. Link: Who can represent a deceased estate | Australian Taxation Office

- How can you tell who the LPR is?

- Ask the client/ the client's lawyer?

- Check:

- Grant of probate from the Supreme Court

- Letter of Administration

- Will - the executor (LPR) will be explicitly named in the deceased person's will

Once we know who the LPR is, ask them to nominate us as their tax agent

If the client LPR is the lawyer -> ask them if they can nominate us straight away -> See Vivian case below, Rockcliff, Seini

If LPR is only the lawyer and they refuse to nominate us = nothing we can do.

If the lawyer refused to nominate us straight away (Loan Norris case), we have to do the procedure below:

- Notify ATO who is the LPR (mostly the wife of the deceased)

- in the form, nominate us as tax agent (see below for details procedure)

See procedures here https://teresatranassociates.freshdesk.com/en/support/solutions/articles/36000600794-notification-of-death-decease-go-to-australia-post

Where there is no LPR i.e. no grant of probate or letters of administration

If client decided not to apply for probate or letters of administration,

then provide the will (if there is one).

ATO can:

- use the will to verify your role in the estate's tax affairs

- add your name to our records, with a note that you are managing the estate's tax affairs.

However, you will not be recorded as the LPR or authorised contact on the deceased person's record. This means there are legal restrictions on the information and funds we can release to you. QC67531

C. ONCE YOU ARE AUTHORISED TAX AGENT

Final tax return for the late [person]

- If the client has a deceased estate (point 1), check with the lawyer for the deceased's estate trust bank account. Update all account details in ATO to the deceased's Trust account.

- If client don't have deceased estate -> check the bank details before update

______________________________________________________________

BELOW ARE CHRIS NOTE ON PREVIOUS CASE

Chris Norris (Jenni)

- background: lawyer didn't let us do ESTATE + didn't want to add us as Tax agent (possibly because you can only have 1 tax agent at a time)

- So when Jenni did the EXECUTOR matter and called ATO to ask for refund, ATO said no and we needed to be added

- we knew Chris norris had some overpaid tax in his income tax account for the surviving wife (loan) to retrieve.

- Jenni asked lawyer to add us to the decease and lawyer refused and made us do it - which is wrong. they must do it.

- but because TT and Jenni didn't understand/know - they tried to do it.

Hence the problems:

- 1st attempt Jenni did Auspost online form and had TT as the LPR - this was a mistake and misread of instructions.

- 2nd jenni then did TAP msg of 3rd party authority form and attachments in C:\Users\TTRAN01\OneDrive - Teresa Tran and Associates\Office sharepoint\INDIVIDUALS\NORRIS CHRIS\OTC\20250513 Request tax credit

- ato replied they want the client (loan) to send it directly to them)

- finally Jenni posted a everything including the notification of death via post to ATO, with the from address being loan on the envelope, and ATO finally accepted.

ROCKLIFF, SEINI (vivian case)

- Vivian emailed the lawyer to get us added to Seini Rockliff profile (not decease estate)

- lawyer complied thus vivian was able to do everything

- however Chris checked

- there is no decease estate because she had no assets

- and when chris check profile, it just looks like this

ATO call

09/03/2026 phone call - brendan titterton, frederick ziems

https://app.clickup.com/t/86cvgx8mc?comment=90160171293604

- Frederick ziems ref # 105 251 628 709 5 fred died in 2021. so by 2026 its locked if you dont do the notification form, no LPR

- Kevin rodgers bad. Didnt do this for Charles HITCHINGS

- Kevin rodgers bad. Didnt do this for Charles HITCHINGS

- Brendan titterton ref#105 251 629 657 8

- 4th March 2026 chris became aware we were kicked out of the account

- 8th March 2026 chris added back and it was okay.

- it will take time for ATO to kick us out

10/03/2026 - vincent ip & Frederick ziems

- Vincent IP ref#105 251 693 325 0

- even though we can add and see them on TAP, we won't be able to do anything until the LPR is updated

- not even general enquiries

- merely updating the decease status on client detail is not enough. You must go through the AustraliaPost process.

- since there is no grant of probate or adminsitration, we have to go through the longer process of having to provide

- evidence of why we didnt go to court to get this stuff

- relationship to decease

- and constantly explanations whenever we need to action

- letter to explain + tfn +

- stat dec

- this guy will probably have to through the mail. dont bother uploading to practice mail

- even though we can add and see them on TAP, we won't be able to do anything until the LPR is updated

- its an unofficial appointment - doesnt mean anything. so you still need the lpr stuff resolved.

- Frederick ziems ref 105 251 699 200 6, definitely no notification of death, therefore no LPR was done

Examples

Hazel BOWNLEE, BEVERLEY

TITTERTON Brendan

IP, VINCENT

- 8th March 2026 chris noticed we were removed and added back now.

- but we will be kicked out again

- issue is parents are overseas.

Frederick ziems

Executor

decease estate

Charles hitchings

estate

raymond phelan

executor

Dale Stobie

but cant view individual

estate

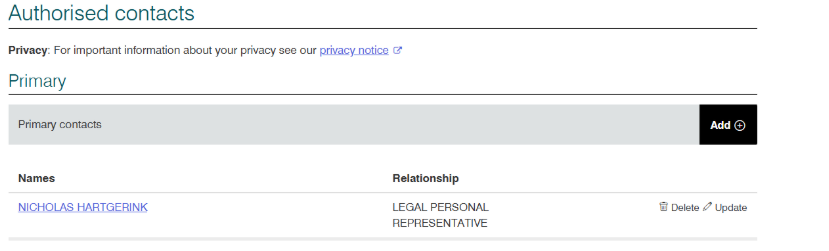

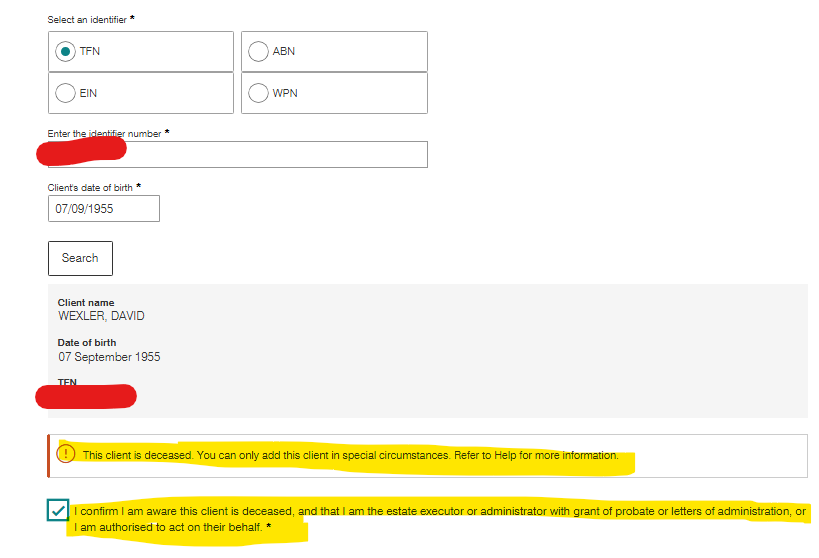

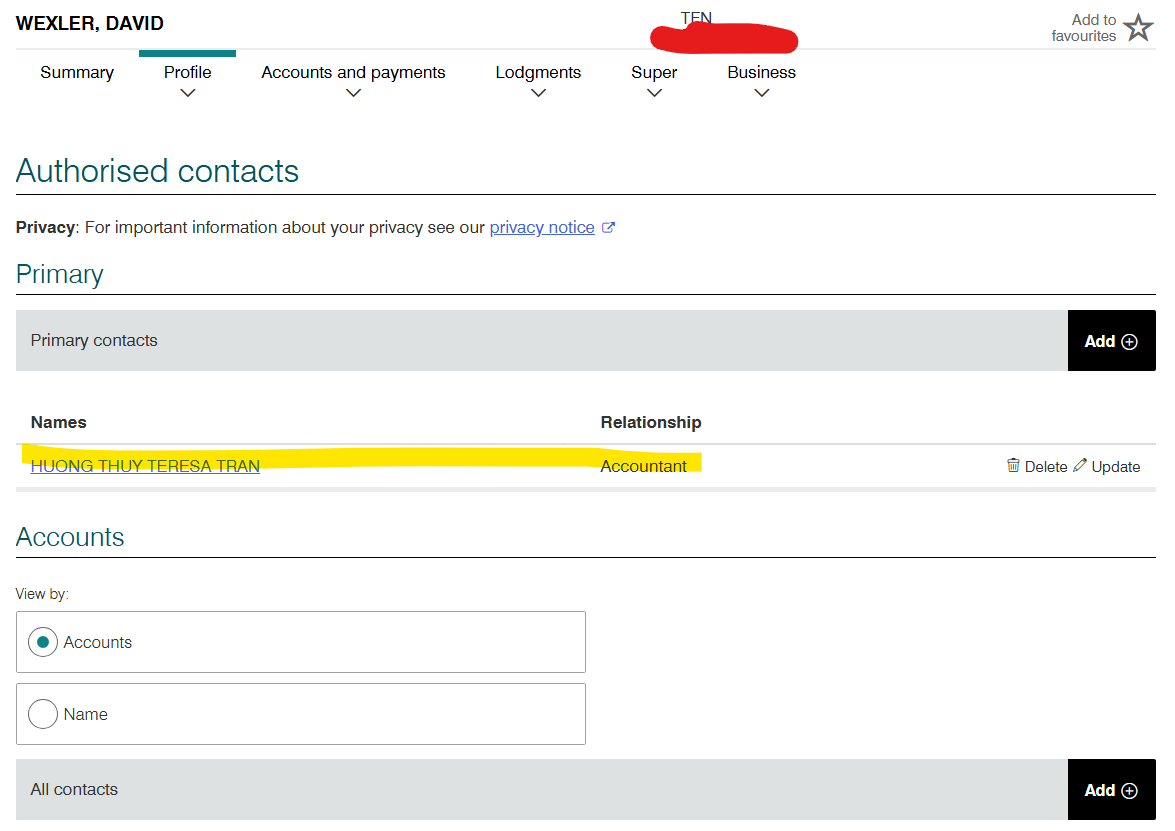

David wexler

- 16/04/25

- sometime this period or before, he died. Therefore he died without doing 2024 and 2025 tax return.

- Wife emailed us to do tax return for 2024 (late) and 2025 (in advance)

- 2024 was lodged end of April

- 25/12/25 2025 was lodged

- 1/4/26

- chris checked TAP and the client is definitely been removed:

- chris later added client back

- chris download the

- income tax account to see what happen to tax refund. there was cancellation - and bank details are cleared. either bank details were wrong or because of death no refund can be issued

- and 2025 noa missing. showing BALANCING ACCOUNT - status in progress

- use this opportunity to download a document to keep a ato correspondence id (download 2024)

- currently system down so chris recorded this 2024 2811400044228

- income tax account to see what happen to tax refund. there was cancellation - and bank details are cleared. either bank details were wrong or because of death no refund can be issued

- communication history down as well

- Millie did call ato and they demand LPR (expected)

- chris check tap authorised contact and found no LPR. Chris added teresa temporarily

- chris checked TAP and the client is definitely been removed: